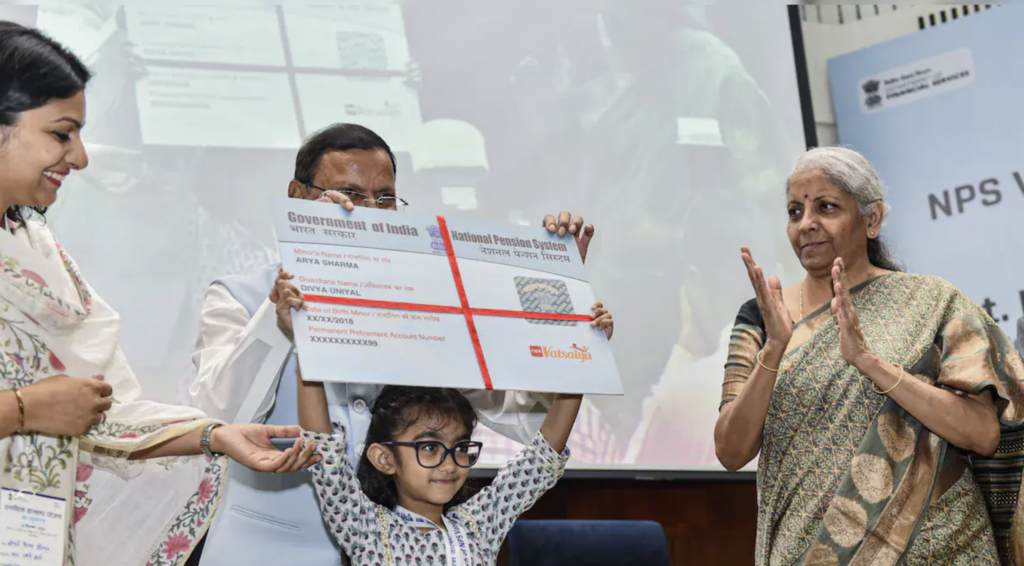

Finance Minister Nirmala Sitharaman unveiled the NPS Vatsalya scheme which is designed to help parents to save for their children’s futures through a pension account on September 18, 2024.

NPS Vatsalya Scheme for Children’s Pension Savings

This initiative enables the parents to invest in a pension scheme that would be tailored as per their minor children, hence promoting long term financial security. The enrolment for the scheme can be done either online or by visiting designated banks or post offices. In order to open an account, the minimum initial contribution of ₹1,000 is must, which is then followed by an annual contribution of the same amount.

Notably, the details of the withdrawal guidelines from the NPS accounts are still being finalized. The finance minister highlighted the competitive returns generated by the National Pension Scheme (NPS) and emphasized the importance of saving for future income.

The scheme is basically an extension of the existing NPS scheme, with the difference that this scheme enables the parents to establish pension accounts for their children under 18 years of age.

Once the child reaches the age of 18, the NPS Vatsalya account shall transition to regular NPS, with pension disbursements commencing at age 60. NPS has amassed approximately 1.86 crore subscribers and an impressive Asset Under Management (AUM) of ₹13 lakh crore over the period of last decade.

The scheme is regulated by the Pension Fund Regulatory and Development Authority (PFRDA), and newly registered minor participants will receive Permanent Retirement Account Number (PRAN) cards. In order to avail the scheme, both the child as well as parent has to be an Indian and all the parties must comply with Know Your Customer (KYC) regulations.

Investment Options and Withdrawal Guidelines

Different investment strategies can be chosen by the investors. By default, the moderate life cycle fund allocates 50% to equity. There are other options as well which include aggressive or conservative lifecycle funds which accordingly allocate funds to equities, corporate debt, government securities, and alternative assets.

As far as withdrawal is concerned, the process allows a maximum of three withdrawals after a 3-year lock-in period, enabling access to up to 25% of contributions for specific needs such as education or medical emergencies.

The child’s NPS Vatsalya account will convert to a standard NPS account upon completing 18 years and if the investment exceeds ₹2.5 lakh at that age, 80% must be used to purchase an annuity, while the remaining 20% can be withdrawn.

If the total investment is ₹2.5 lakh or less, a full lump-sum withdrawal is permitted. In the unfortunate event of the contributor’s death, the entire investment will be returned to the designated guardian.

Comments are closed.