Invest just Rs 7 per day, get Rs 60,000 annually in old age! Know the complete calculation of Atal Pension Yojana

Atal Pension Yojana Benefits: The government is working on different fronts for the general public of the country, especially the poor and the deprived. To move towards creating a universal social security system, the government announced three social security schemes linked to the insurance and pension sectors in the Budget 2015-16. In this direction, Atal Pension Yojana was started on 9 May 2015. This scheme is applicable from 1 June 2015.

However, the objective with which the government had started this scheme, its impact is rarely seen even today. The real reason for this is that very few people know about this scheme. This is the reason why most of the eligible people are also deprived of the benefits of this scheme. There are some people who are aware of this scheme. But they do not know how to avail the benefits of this scheme. So let us understand all the information related to this scheme in very simple language.

What is Atal Pension Yojana?

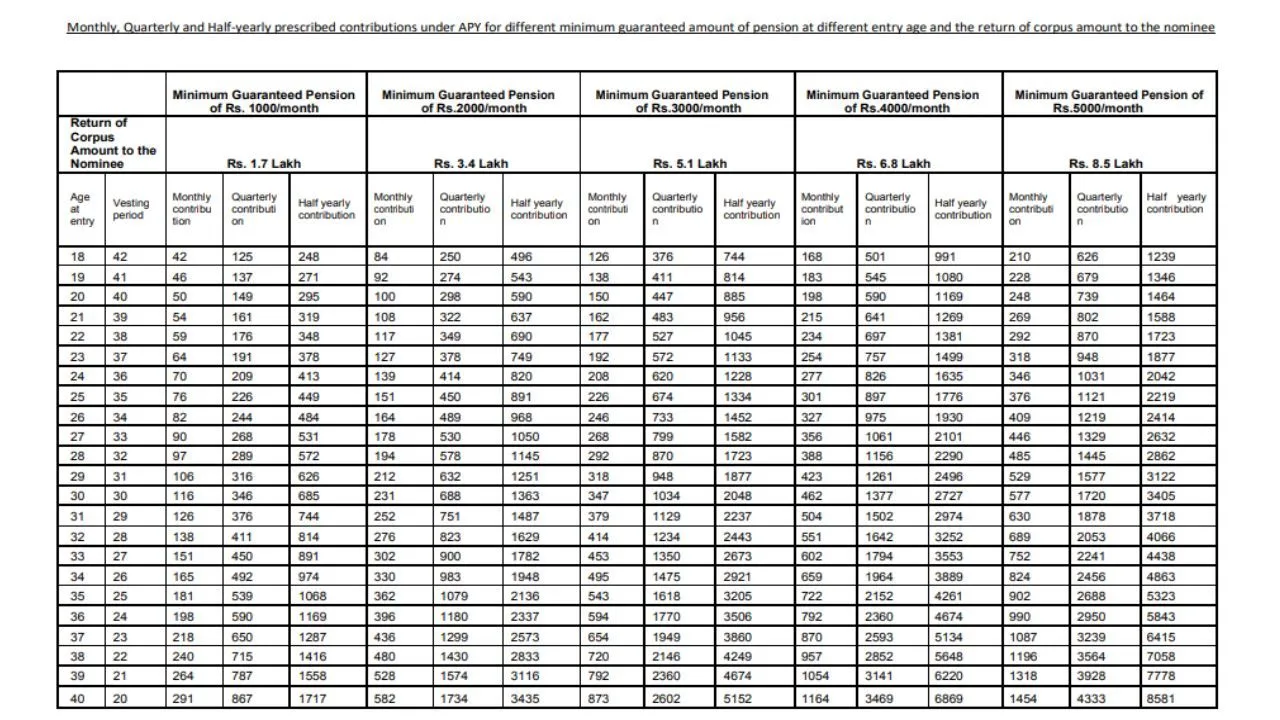

Atal Pension Yojana (APY) is a social security scheme run by the Government of India, whose main objective is to provide financial security to unorganized sector workers and poor citizens in old age. Under this scheme, after the age of 60 years, a monthly pension of Rs 1,000 to Rs 5,000 is guaranteed every month.

Benefits of Atal Pension Yojana

Atal Pension Yojana is a pension system based on voluntary periodic contribution, under which the subscriber will get the following benefits-

1. Benefit of minimum pension guaranteed by the Central Government

Under Atal Pension Yojana, every subscriber will get a Central Government guaranteed minimum pension of Rs 1000, 2000, 3000, 4000 or 5000 every month from the age of 60 years till death.

2. Benefit to spouse after death of subscriber

After the death of the subscriber, his/her spouse has the right to receive the same pension amount as the subscriber till the death of the spouse.

3. Pension rights to the subscriber’s nominee

After the death of both the subscriber and the spouse, the nominee of the subscriber will be entitled to receive the pension amount accumulated up to the age of 60 years of the subscriber.

On death of the subscriber before the age of 60 years

In case of death of the subscriber (before the age of 60 years), the spouse of the subscriber has the option to continue to contribute to the subscriber’s APY account for the remaining period till the original subscriber turns 60 years of age. Then the spouse of the subscriber will get the same pension amount as the subscriber gets, till the death of the subscriber. After the death of both the subscriber and the spouse, the nominee of the subscriber will be entitled to receive the pension amount accumulated up to the age of 60 years of the subscriber.

The minimum pension is guaranteed by the government, i.e. if the accumulated amount based on contributions earns less than the expected return on investment and Minimum Guaranteed Pension If there is not enough to give, then the Central Government will make up the shortfall. Or if the return on investment is high, the subscriber will get more pension benefits.

Eligibility for Atal Pension Yojana

- All those people who have a savings bank account can avail the benefits of Atal Pension Yojana.

- The minimum age to join Atal Pension Yojana is 18 years and maximum age is 40 years.

- Any citizen who is or has been an income tax payer after October 1, 2022, is not eligible for this scheme.

How much money is deducted from Atal Pension Yojana?

- The minimum age to join Atal Pension Yojana is 18 years and maximum 40 years. The age for leaving and starting pension is 60 years.

- Subscriber’s contribution to Atal Pension Yojana will be made through ‘auto-debit’ of the fixed contribution amount. Through this facility, the savings of the subscriber will be transferred to the bank account every month, every three months or every six months.

- The subscriber is required to contribute the prescribed contribution amount from the age of joining Atal Pension Yojana till the age of 60 years.

APY withdrawal and pension payment

On completion of 60 years, the subscriber will receive a guaranteed minimum monthly pension, or a higher monthly pension depending on the investment returns. In certain circumstances, i.e. in the event of death of the beneficiary or specified illnesses, as prescribed in the Pension Fund Regulatory and Development Authority (Exit and Withdrawal under the National Pension System) Regulations, 2015, the pension amount accumulated so far before the age of 60 years will be paid to the nominee or subscriber, as the case may be.

What if I leave Atal Pension Yojana midway?

If any subscriber, who Atal Pension Yojana If a subscriber has taken Government co-contribution under APY and wants to leave it voluntarily before the age of 60 years, then only his contribution to APY and the net actual interest received on his contribution (after deducting the account maintenance charge) will be refunded, whereas the Government co-contribution and interest received on Government co-contribution are not refunded to such a subscriber.

Also read: Post Office RD: Start investing with just ₹ 100, you will get huge fund on maturity; Know the rules regarding interest and loan

How to close Atal Pension Yojana?

If for some reason you want to close Atal Pension Yojana (APY), then you can get it closed through a very easy process. For this you will have to go to your bank or post office from where you had opened your savings bank account. Go there and fill the ‘Atal Pension Yojana Voluntary Exit Form’ Fill it and submit it along with photocopies of your PRAN card, Aadhar card, and bank passbook.

Comments are closed.