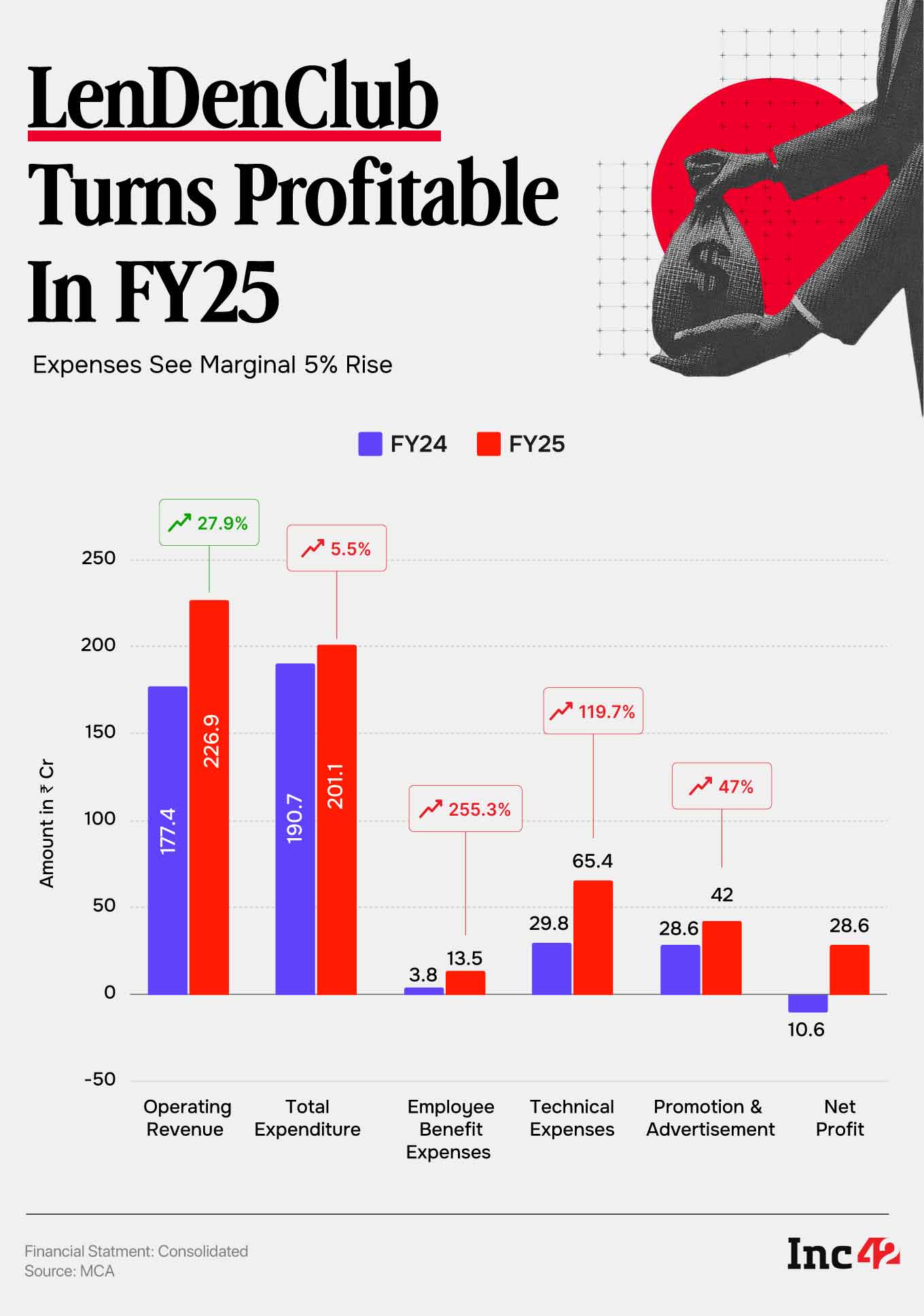

The startup returned to the black in FY25, reporting a net profit of ₹28.6 Cr compared to a ₹10.6 Cr net loss in FY24

LenDenClub’s expenses saw a marginal 5% rise to ₹201 Cr in FY25 from ₹190.7 Cr in the previous fiscal year

Currently, around half of the startup’s revenue comes from its LSP business, while its P2P business rakes in 40%

Peer-to-peer (P2P) lending startup LenDenClub is eyeing nearly 50% YoY revenue growth in the ongoing financial year (FY26) after returning to the black in FY25.

“We will close this financial year with around ₹330 Cr to ₹350 Cr in revenue. EBITDA margin will also improve during the year as we scale further,” cofounder and CEO Bhavin Patel told Inc42, without giving a bottom line estimate for FY26.

After a tumultuous few years due to RBI’s crackdown on P2P lending starting 2024, the startup bounced back in the previous fiscal year to report a net profit of ₹28.6 Cr in FY25 compared to a net loss of ₹10.6 Cr in FY24. The startup had turned profitable in FY22 but slipped into the red following RBI’s regulatory changes.

Operating revenue rose almost 28% to ₹227 Cr in FY25 from ₹177.4 Cr in the prior financial year. Including other income of ₹14.48 Cr, total revenue during the fiscal year stood at around ₹241.4 Cr.

“There is a growth in the overall platform operations and that growth brings economies of scale. As a result, our operations or the compliance costs are not increasing the same way as the business is increasing,” Patel said.

The startup earns revenue commission charges, registration charges and loan processing fees.

In FY25, the startup’s expenses saw a marginal 5% rise to ₹201 Cr from ₹190.7 Cr in the prior fiscal year. Here’s a breakdown of the startup’s expenses during the fiscal year:

Employee Benefit Expenses: LenDenClub spent ₹13.5 Cr under this head during the year, a 3.5X jump from ₹3.8 Cr spent in FY24.

Technical Expenses: The expenses for technical assistance, which generally includes IT infrastructure, SaaS subscriptions and other technical services, rose 2.2X during FY25 to ₹65.4 Cr from ₹29.8 Cr spent in the previous year.

Promotion & Advertisement: This was a significant expenditure for LenDenClub during the year, jumping 47% to ₹42 Cr from ₹28.6 Cr spend in FY24.

Credit Bureau Charges: Expenses under this head jumped 3.6X in FY25 to ₹5.3 Cr from ₹1.1 Cr spent in FY24 owing to higher number of credit checks undertaken by the startup as a lending service provider (LSP).

Zooming Into LenDenClub’s Business

Apart from a P2P lending platform, LenDenClub also operates as an LSP connecting lenders and borrowers. It also acts as a technology service provider (TSP) for banks and NBFCs. According to Patel, the LSP business, called Instamoney, has picked up considerably in the past few years.

Currently, around half of the startup’s revenue comes from its LSP services, while 40% is generated through the P2P platform. The remaining revenue comes from the TSP service business. The startup earns revenue through commission earned from lending partners and fees charged to borrowers at the time of borrowing and paying back.

On the P2P front, LenDenClub connects lenders and borrowers, and helps with historical risk data to understand the probability of default along with providing collection support, agreement facilitation and escrow transactions support.

The RBI tightened its noose around P2P platforms in 2024, banning them from being advertised as investment products. It issued strict regulatory guidelines for such platforms, bringing them under the ambit of a regulated entity. It introduced lending and borrowing caps, T+1 escrow settlements (requires funds in escrow accounts to be transferred within one business day of receipt to prevent pooling funds and park-now-withdraw-later offers), fixed platform fees and zero cross-selling of unrelated products.

The regulatory changes have made the P2P lending model clearer and more transparent, providing clarity to both users and platforms by removing ambiguity, Patel said.

“The earlier business model was more risky for the platform because of whatever marketing was happening or how the operations were running. The new model is super transparent like an exchange model,” the cofounder noted.

Founded in 2015 by Patel and Dipesh Karki, the Mumbai-based startup claims to have disbursed loans worth ₹18,440 Cr till date, hosting 41.63 Lakh lenders and 3.64 Cr borrowers. Its non-performing assets (NPA) stood at 3.53% as of February 2026. During the month, it disbursed 2.22 Lakh loans, and over 74% of them were worth less than ₹1 Lakh.

LenDenClub has raised close to $12 Mn till date from investors like Artha Ventures, Venture Catalysts, Tuscan Ventures, CRED’s Kunal Shah, among others.

According to Patel, the startup doesn’t require additional capital infusion. However, it might plan to list publicly or undergo a private placement round to provide liquidity to early investors. Such plans will only materialise after the startup achieves ₹100 Cr net profit, he added.

LenDenClub competes with the likes of Lendbox, Finzy, Fello, IndiaP2P, iLend, and Faircent in the P2P lending segment.

Comments are closed.