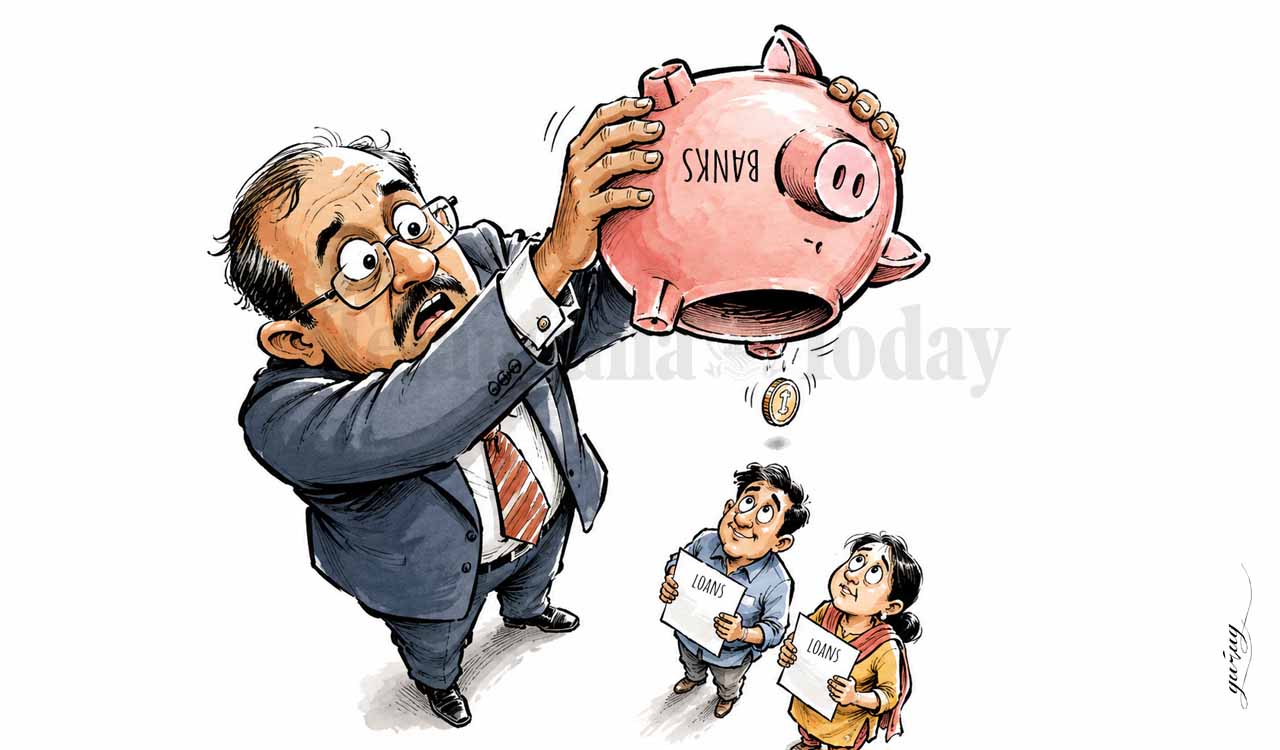

While financialisation is strengthening capital markets, it is weakening low-cost deposit base that has long sustained bank lending and profitability

Updated On – 30 June 2026, 12:04 AM

Illustration: GuruG

By Dr Philip MP, Poola Dharshan Kumar Reddy

For decades, bank deposits were the default savings choice for Indian households. That habit, however, has steadily changed over time. Investments in equities, insurance and pension funds, once ancillary to household balance sheets, have become increasingly important components of household financial wealth.

Among the non-traditional avenues, the shift towards capital market instruments has been particularly pronounced. As noted in the Economic Survey 2025-26, the share of equity-oriented savings in annual household savings rose from around 2 per cent in FY12 to more than 15 per cent in FY25. In contrast, the share of deposits fell from 57.9 per cent to 35.2 per cent during the same period.

Key Drivers

Mutual funds (MFs), driven largely by the rapid growth of Systematic Investment Plans (SIPs), have been the principal force behind this shift. SIPs allow investors to invest fixed sums at regular intervals, often starting with as little as Rs 500 a month, without having to worry about when to enter or exit the market. Monthly SIP inflows have risen sharply, with average monthly contributions increasing more than sevenfold from under Rs 4,000 crore in FY17 to over Rs 29,000 crore in FY26, according to data released by the Association of Mutual Funds in India (AMFI).

While household portfolio diversification towards equities has coincided with a steady increase in SIP inflows, the declining significance of deposits in household savings has been reflected in a substantial squeeze on low-cost current and savings account (CASA) deposits, along with subdued overall deposit growth. RBI data show that the CASA share in total deposits fell from around 44 per cent in March 2023 to 41.6 per cent in March 2024, and further to 37.9 per cent by December 2025.

Aspirational Middle-class

The changing composition of household savings reflects how India’s aspirational middle-class is increasingly prioritising wealth creation over mere capital protection. With deposit rates remaining relatively low and inflation eroding purchasing power, traditional deposits no longer appear sufficient for long-term wealth creation. Households are therefore becoming more willing to take greater financial risks in pursuit of higher returns.

Besides rising incomes, improving financial literacy, a young demographic profile, expanding digital connectivity, and sustained investor-awareness campaigns have all contributed to this shift. In many ways, the growing preference for equity- based instruments is a positive development. When households channel a larger share of their savings into market-linked assets, it strengthens capital markets, broadens ownership and creates a more informed investor base. Greater retail participation reduces excessive dependence on institutional capital and supports the long-term financing needs of the economy.

This transformation in household savings pattern carries implications not only for household investment behaviour and the broader financial architecture but also for the intermediation role of banks and their long- term sustainability.

The CASA share in total bank deposits declined from around 44 per cent in March 2023 to 37.9 per cent by December 2025, underscoring the growing funding challenge for India’s banking system

The moderation in deposit growth in recent years has coincided with strong credit expansion. According to Reserve Bank of India data, the loan portfolio of scheduled commercial banks increased by 20.6 per cent in FY24, while deposits rose only by 13.5 per cent. A similar divergence persisted in FY26, when bank credit expanded by 16 per cent compared with deposit growth of 13.4 per cent.

As credit growth continued to outpace deposit growth, the banking system’s credit-deposit (C-D) ratio – the metric measuring the proportion of deposits deployed as loans — rose from around 76 per cent in the fourth quarter of FY23 to about 82 per cent in March 2026, indicating mounting pressure on the funding side of the banking system. Earlier, banks relied heavily on deposits, especially low-cost current and savings account balances, to fund lending.

Competition for Funds

However, as household savings increasingly flow into market-linked instruments, banks face higher competition for funds. To sustain credit growth, they have raised fixed deposit rates and relied more on interbank liabilities and market borrowings, particularly certificates of deposit (CDs). While these sources provide additional liquidity, they are costlier and less stable than traditional retail deposits. The result is pressure on net interest margins (NIMs) – the spread between the interest banks earn on loans and the interest they pay on deposits and other liabilities – a key measure of their core profitability.

According to a recent McKinsey analysis using RBI data, banking sector NIMs declined from 3.3 per cent in FY24 to 3.1 per cent in FY25, while funding costs rose from 4.4 per cent to 4.6 per cent of average assets. The implications extend beyond bank profitability. If credit growth continues to outpace deposit growth, funding constraints could eventually moderate lending and create liquidity pressures that weaken the transmission of monetary policy. Early signs of such moderation emerged in FY25, when credit growth slowed amid tighter regulatory norms.

These developments should not be viewed as a reason to resist financialisation. A more financially aware population and wider participation in formal markets are signs of economic maturity. However, the Indian banking system must adapt to this changing savings environment. Deposits can no longer be assumed to flow automatically into banks. To attract and retain household savings, banks will need to strengthen their digital capabilities, offer more flexible deposit products and compete more effectively with fintech firms and payment platforms.

For younger customers with multiple investment options, seamless mobile-based access, superior customer experience and efficient digital onboarding may become as important as interest rates themselves. While banks have already initiated some of these measures and deposit mobilisation has improved, the pace of growth remains insufficient to fully support the expanding credit needs of the economy.

Sustained efforts to enhance customer convenience and offer attractive real returns on deposits will be essential to expand the deposit base in a structurally durable manner. Policymakers must also recognise that household finance in India is undergoing a fundamental transformation. As financial awareness and market participation deepen, the importance of investor protection, financial literacy and financial stability becomes even greater. The challenge is not merely to promote deposit growth, but to ensure balance and stability within the financial system as household savings patterns continue to evolve.

(Dr Philip MP is Professor and Poola Dharshan Kumar Reddy is student, Department of Economics, Christ (Deemed to be University), Bengaluru)

Comments are closed.