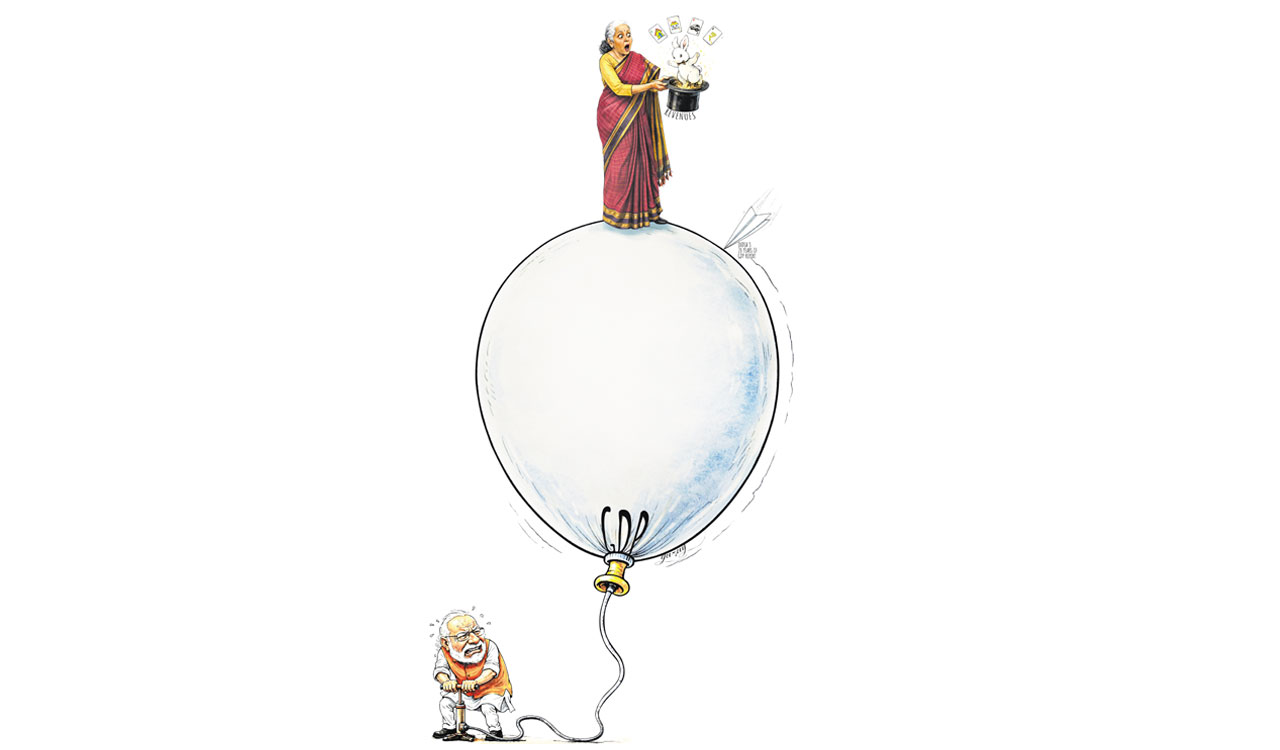

India’s GDP growth between 2012 and 2023 may have been overstated, with actual expansion closer to 4–4.5% a year than the official estimate of about 6%, says a working paper by Abhishek Anand, Josh Felman and Arvind Subramanian

Published Date – 15 March 2026, 01:06 AM

A new working paper argues that India’s GDP growth was significantly misestimated, underestimated during the boom years between 2005 and 2011, and overstated during the years that followed, from 2012 to 2023.

The findings are based on a March 2026 working paper titled ‘India’s 20 Years of GDP Misestimation: New Evidence’ by Abhishek Anand, visiting fellow at the Madras Institute of Development Studies, Josh Felman, principal at JH Consulting, and Arvind Subramanian, senior fellow at the Peterson Institute for International Economics, published by the institute. The authors examine the GDP methodology introduced in January 2015, initially applied to the post 2011–12 numbers and later to the historical series.

Revised Methodology

The study comes at a time when the government introduced a revised GDP methodology in February 2026. The authors highlight two main reasons for the revision: first, to update the weights of various goods and services, a step long overdue given the significant changes in India’s economy since the weights were last set in 2011–12; and second, even more importantly, to correct methodological flaws that economists and statisticians had identified over the years.

According to the paper, India’s economy actually experienced a strong boom between 2005 and 2011, with growth rates likely 1-1.5 percentage points higher than the official estimates for those years. However, between 2012 and 2023, growth may have been overstated by 1.5-2 percentage points annually, suggesting the economy expanded more slowly than official numbers indicate. Further, it says the economy grew around 4–4.5% per year between 2011 and 2023, as compared with the official figure of roughly 6%.

With these adjustments, the growth story changes significantly — boom in the early 2000s followed by a slowdown after the global financial crisis and domestic shocks.

The study also draws on a backcasting exercise, which re-estimated historical GDP using the 2015 methodology applied to earlier years. The backcasting highlights that the boom in the mid-2000s was more pronounced than officially reported, and the subsequent slowdown more severe, offering a revised picture of India’s economic trajectory.

Problems in Methodology

The study identifies two main methodological problems in the GDP calculations introduced in 2015.

• Informal sector measurement

India’s informal sector makes up about 44% of the economy, but since reliable data are limited, statisticians used indicators from the formal corporate sector as a proxy. That assumption worked reasonably well earlier because both sectors tended to move together. But after 2015, several shocks disproportionately hurt informal businesses:

• The 2016 demonetisation, which removed 86% of the currency in circulation

• Introduction of Goods and Services Tax (GST)

• Covid-19 pandemic

These events hit the informal enterprises most, such as small traders, workshops, and local services. Yet GDP estimates assumed both sectors were performing similarly, which likely overstated economic activity.

Data from surveys such as the Periodic Labour Force Survey (PLFS), Annual Survey of Industries, and the Annual Survey of Unincorporated Sector Enterprises show that while formal sector sales continued to grow robustly after 2015, informal sector sales lagged, averaging only 6.8% annually compared with 10% in the formal sector. This divergence was not captured in official GDP, further overstating growth.

Moreover, the MCA-21 corporate database, which expanded the sample of firms used to calculate GDP, included many with unaudited accounts, firms that were non-traceable, misclassified, or closed. “The assumption that the informal sector was doing as well as the formal sector, during a period when it was actually falling far behind, seems to have inflated the estimates of GDP growth.”

• Inappropriate price deflators

The second problem relates to how economists convert nominal values (current prices including inflation) into “real” growth (inflation-adjusted growth) figures. In many sectors, GDP calculations used the Wholesale Price Index (WPI) as a deflator. However, WPI is heavily influenced by commodity prices such as oil and often reflects input costs (raw material prices) rather than the prices consumers pay for finished goods and services.

Between 2011 and 2025, these input prices grew much more slowly than consumer prices. As a result, the GDP deflator may have understated actual inflation, making real growth appear higher than it actually was.

Ideally, economists use double deflation, which separately adjusts output and input costs using appropriate price indices to derive real GDP growth. But between 2011 and 2025, WPI inflation was on average 2.2 percentage points lower than the Consumer Price Index (CPI). This reliance on WPI likely led to an overestimation of real GDP growth during this period.

Mismatch: Economic indicators, GDP

The authors focused on six ‘well‐measured’ macro indicators: exports of goods and services, bank credit (excluding food credit), index of industrial production (IIP), electricity, tax revenues, and corporate sales.

The study highlights a clear mismatch between official GDP data and several broad economic indicators. According to GDP figures, India’s economy grew steadily over the past two decades, with growth easing only slightly from an average of 6.9% between 2004 and 2011 to about 6.1% between 2012 and 2024. However, other indicators suggest a much sharper slowdown after the mid-2000s boom.

Before 2011, these indicators moved closely with GDP growth. But after the new methodology was introduced in 2015, the correlation weakened sharply. The authors observed this breakdown in India and across countries, indicating that post-2011 GDP growth was likely overestimated

For example, during the earlier boom period (2004-2011):

1. Real credit grew about 15.6% annually

2. Exports rose 13.9%

3. Industrial production increased 16.1%

4. Direct tax revenues expanded at around 13% annually

But during 2012-24, these indicators slowed sharply.

1. Credit growth fell to 5.6%

2. Export growth dropped to 5.4%

3. IIP growth declined to 2.9%

4. Direct tax revenue growth slipped to 7%

The authors argue that when several major indicators weaken together, they likely reflect changes in the overall economy. The trend reveals India’s growth slowed significantly after the mid-2000s boom, despite GDP showing only a modest deceleration.

Such divergence raised questions among economists. In 2016, demonetisation accelerated GDP growth to an eye‐popping annual rate of 8.3%. It resurfaced in 2019, when a credit crunch in India’s nonbank financial institutions caused only a minor blip in growth. By June 2025, with private investment and job creation weak but GDP still booming, and the IMF giving India’s GDP methodology a mere C grade, two former officials of the national statistical agency publicly remarked that “something does not add up.”

The Big Gap

“The overestimation of long‐run growth suggests that as of 2025, the level of real GDP is overstated by about 22 per cent and the level of real consumption by about 31 per cent,” say the authors.

They also highlight subtle effects: GDP misestimation magnifies its impact on consumption. When GDP is revised, expenditure figures — especially consumption — must be adjusted. The backcasting exercise cut 2005–11 GDP growth by 1.7 percentage points and consumption growth by 2.3 percentage points, making consumption during boom period slightly lower than in the following decade, contrary to household survey findings. If correct, this would mean that India’s economy is somewhat smaller and average living standards lower than official figures indicate.

Despite the potential revisions, the authors emphasise that India would still rank among the seven or eight fastest-growing economies globally during 2011 and 2023. National pride may be justified, but it does not require a statistical crutch, they say.

Quoting Robert Solow, the authors note, “productivity growth can sometimes be seen everywhere except in the statistics.” In India, they add, growth has sometimes been evident nowhere but in the GDP statistics — and occasionally everywhere but in the GDP statistics.

Rising tax revenues may not signal boom

During the boom years 2004–2011, non-oil tax revenues grew at about 18.1% annually, in line with strong nominal GDP growth (increase in economy’s total output measured in current prices, without adjusting for inflation). In the following period, 2011–2019, tax growth slowed to 10.3% as economic growth moderated.

The sharpest surge in tax collections was after the pandemic, when the tax-to-GDP ratio rose significantly. However, the authors say this increase was driven less by broad economic expansion and more by changes in the pattern of income and spending. Rapid growth in high-income sectors such as financial markets, real estate and Global Capability Centres boosted personal income tax receipts. The share of individuals earning over Rs 1 crore rose from about 8% to nearly 18%. At the same time, higher spending on luxury goods like SUVs increased GST collections, reflecting a K-shaped recovery concentrated among higher-income groups, rather than signalling broad-based economic expansion.

Getting numbers right matters

Misestimated GDP numbers lead businesses to misinvest, households to overspend, and the central bank to keep monetary policy tight. Inaccurate numbers result in misguided policy decisions — government cannot respond to problems it cannot see.

Individual indicators may fluctuate for idiosyncratic reasons, including methodological flaws. However, when all key indicators move in the same direction, they reflect the true state of the economy.

Comments are closed.