Thinking of saving tax by gifting money to your wife? So be careful! This ‘clubbing’ rule of income tax will ruin your planning

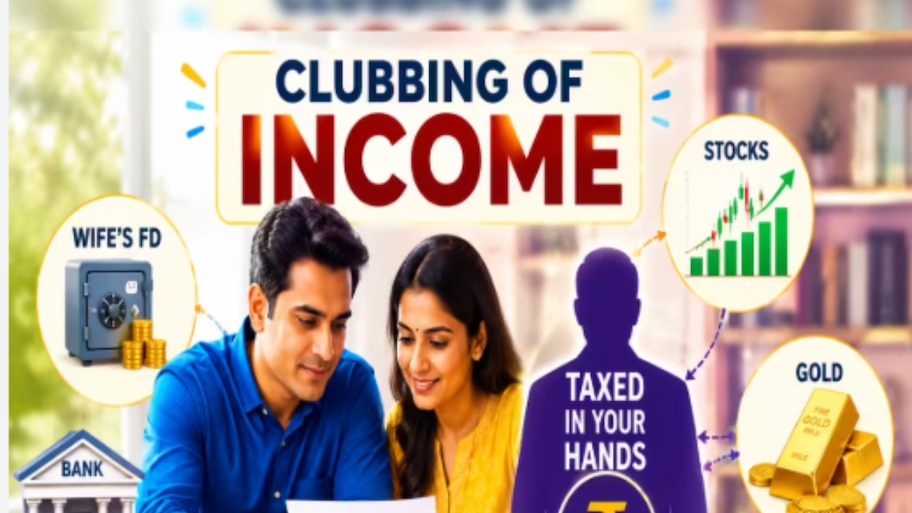

Many times people adopt a very common method to reduce the tax burden—they transfer or gift a part of their hard-earned money to their wife’s bank account. After this the wife invests that money in fixed deposit (FD), gold, mutual fund or stock market. If you are also planning something similar, then wait! A very strict income tax rule can spoil your entire planning. According to the Income Tax law, whatever profit or interest you get from this investment made in the name of your wife, the tax on it will not have to be paid by your wife but directly by you (husband).

The Income Tax Department keeps a close watch on such cases under ‘Clubbing of Income’. Its direct objective is to prevent attempts to evade tax by transferring property or money in the name of family members. Let us understand in simple language the complete details behind this rule and the legal ways to avoid it from the perspective of an expert reporter.

What is Section 64 of the Income Tax Act? Understand the game of ‘clubbing of income’

There is a provision for ‘clubbing of income’ under section 64 of the Income Tax Act. Simply put, it means that under certain circumstances, the income earned by someone else is clubbed with your total annual income and then tax is collected on it as per your tax slab.

If a person gifts any amount of money to his wife and the wife invests that amount in any financial scheme like FD, gold, shares or mutual fund, then the annual interest, dividend or capital gain received from that investment will legally be considered as the income of the husband.

When do clubbing rules not apply? Know these important exceptions

This strict income tax rule also includes some saving exceptions where the clubbing provisions become completely ineffective:

Own professional qualifications: If your wife earns her own money on the basis of any technical, business or professional qualification, then the rule of clubbing will not apply to her earnings.

Working Professionals: For example, if the wife earns income as a doctor, engineer, Chartered Accountant (CA), freelancer or based on any of her special arts, then that income will be considered entirely her own and she will have to pay tax on her PAN card herself.

3 completely safe and legal methods of tax planning

If you want to do tax planning in a completely legal manner while staying within the rules, then the Income Tax Act gives you these best options:

Gift money to parents: If you gift money to your parents instead of your wife and they invest that amount in senior citizen FD or other safe investments, then the income from it will be considered theirs. Since clubbing rules do not apply, you can legally save tax if your parents fall in a lower tax slab.

Wedding Gifts: There is no tax on cash or property received from relatives and friends on the auspicious occasion of Hindu marriage or any other marriage. If the amount of gifts received at that wedding is invested somewhere, then the income from it is also taxable in the hands of the recipient (whose marriage took place), there is no clubbing on this.

Magical option to invest in PPF: If you deposit money in the Public Provident Fund (PPF) account in the name of your wife or minor child, then the annual interest received on it is completely tax-free by law. Since there is no tax on interest, the clubbing rule has no adverse effect here. However, keep in mind that the maximum limit of investment per PPF account in a financial year is only ₹ 1.5 lakh.

Comments are closed.