Star Health claim rejection cases and rising industry-wide complaint data raise a larger question: Are policyholders being told enough about why their claims are denied? Health insurance for many policyholders is about trusting in someone. Year after year, premiums are paid with the expectation that, when a medical emergency occurs, the insurer will provide financial assistance. But for a growing number of policyholders, the real battle begins after they file a claim. But government figures submitted to Parliament show disputes over claims are becoming a major problem throughout the insurance industry. Simultaneously, policyholders of Star Health & Allied Insurance have been sharing their woes on social media and have a unified complaint: it’s not only claim rejections but also the lack of a detailed reason behind those rejections.

Looking at complaint data, social media, and customer feedback, we are questioning whether policyholders have adequate information to understand and dispute claim rejections.

The number of complaints registered against insurers went up from 2,02,640 in FY23 to 2,57,790 in FY25, as per data provided by the Ministry of Finance in Parliament.

As per IRDAI data:

| Financial Year | Total Complaints |

|---|---|

| FY23 | 2,02,640 |

| FY24 | 2,15,569 |

| FY25 | 2,57,790 |

More importantly, claim-related issues account for nearly half of all insurance complaints.

| Financial Year | Claim-Related Complaints | Share of Total Complaints |

|---|---|---|

| FY23 | 84,009 | 41.45% |

| FY24 | 1,00,996 | 46.85% |

| FY25 | 1,26,412 | 49.04% |

The trend suggests that disputes involving claims are becoming an increasingly dominant source of consumer dissatisfaction within the insurance sector.

The Most Common Complaint? Claims Not Being Disposed Of

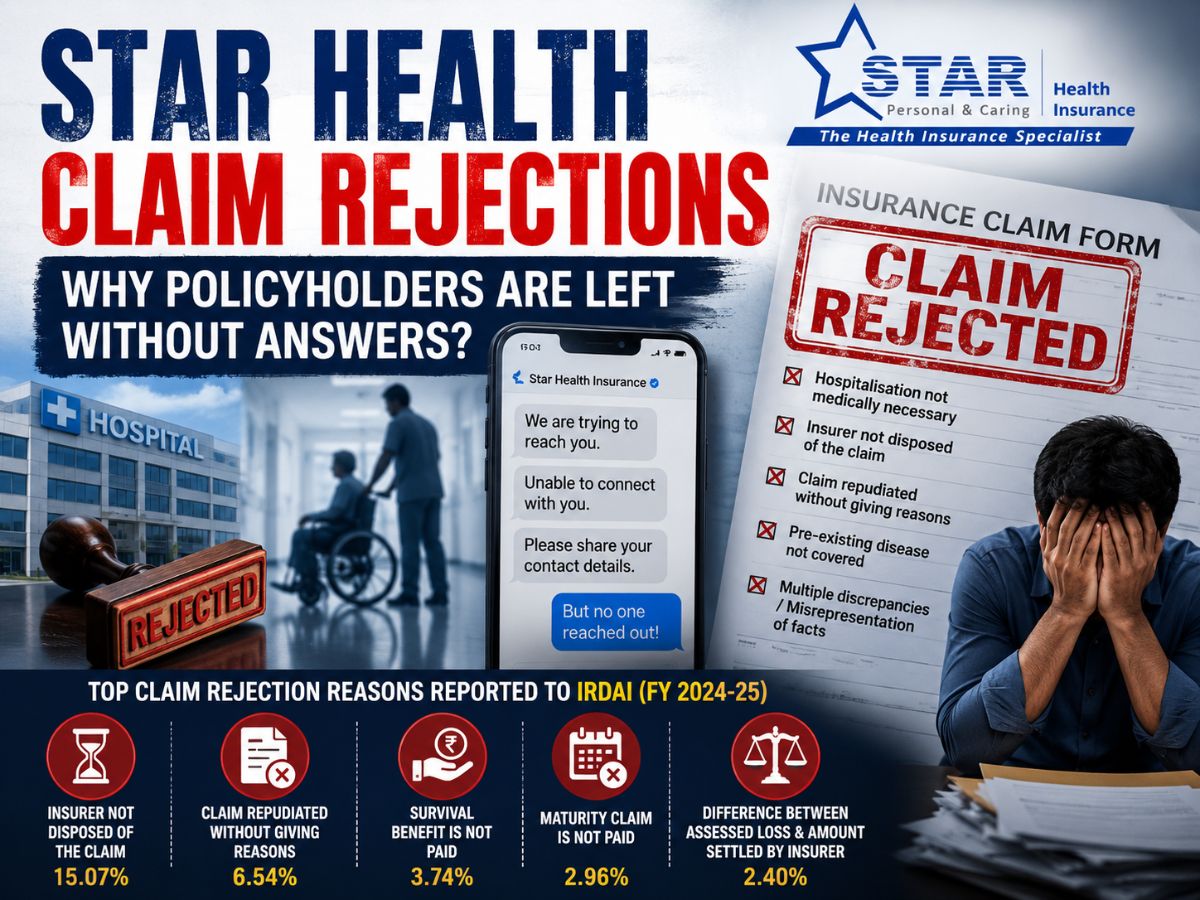

The Finance Ministry revealed that “the insurer did not dispose of the claim” has remained the single largest reason for complaints for three consecutive years.

| Top Complaint Category | FY23 | FY24 | FY25 |

|---|---|---|---|

| Insurer not disposed of claim | 15.20% | 13.99% | 15.07% |

| Claim repudiated without giving reasons | 3.15% | 5.34% | 6.54% |

| Survival benefit not paid | 4.35% | 3.77% | 3.74% |

| Maturity benefit not paid | 3.48% | 3.49% | 2.96% |

| Difference between assessed loss and settlement | 1.06% | 2.17% | 2.40% |

One statistic stands out. Complaints relating to “claim repudiated without giving reasons” more than doubled from 3.15% in FY23 to 6.54% in FY25.

That increase becomes particularly significant when we view it alongside the experiences policyholders are sharing online.

Star Health’s Grievance Numbers Have Been Rising Since FY ’23

Among non-life insurers, Star Health & Allied Insurance Company has consistently ranked among the companies receiving the highest number of grievances.

The numbers have climbed sharply over the past three financial years.

| Financial Year | Complaints Against Star Health |

|---|---|

| FY23 | 12,465 |

| FY24 | 16,572 |

| FY25 | 20,527 |

That represents an increase of approximately 65% in just two years.

Star Health Insurance complaints alone in FY25 were more than those of several big players like Niva Bupa, ICICI Lombard, HDFC Ergo and New India Assurance.

The number of grievances alone does not prove Star Health wrongful claim rejection and can be a function of the size of the business and the size of its customer base, but the upward trend is hard to ignore.

The real question is why the number of complaints continues to grow despite multiple regulatory efforts aimed at improving the way claims are being settled and protecting policyholders.

A Pattern Is Emerging on Social Media

NewsX reviewed several social media posts from Star Health policyholders who publicly questioned claim rejections, delayed settlements or requests for clarification.

A recurring pattern appeared in numerous instances.

After policyholders posted complaints publicly, Star Health’s official social media accounts often responded by stating that the company had attempted to contact the customer but had been unable to reach them.

However, several policyholders claimed the opposite.

Some customers alleged that they never received any meaningful communication from the insurer explaining the Star Health Insurance claim rejection. Others said they continued contacting the Star Health consumer panel, grievance teams and chatbots seeking answers but repeatedly received the same generic response that the claim had been rejected.

The contradiction creates a difficult question.

Where did the communication breakdown occur? The insurer says it’s trying to reach customers, and customers say they’re actively trying to reach the insurer.

But more importantly, why do policyholders still say they cannot get detailed written explanations of claim decisions?

The Ritesh Chhajed’s Star Health Insurance Claim Rejection Case

One such case is that of Dr Ritesh Chhajed, who was denied reimbursement by Star Health for the treatment of his seven-year-old son’s pneumonia.

The rejection letter cited “various discrepancies” and “misrepresentation of facts”.

But Chhajed told NewsX that even after filing grievances and repeatedly asking for details, he was never told what those discrepancies even were.

He also said no detailed written explanation was provided despite repeated requests.

This case poses a major question.

If an insurer finds discrepancies in the medical records that are serious enough to justify a Star Health Insurance claim denial, should those discrepancies be clearly delineated and brought to the policyholder’s attention?

Without such details, customers may struggle to understand the basis of the rejection or contest it effectively.

Also Read: Star Health Insurance Claim Rejected For 7-Year-Old’s Treatment, Father Shares Ordeal | Exclusive

Another Case: Fever Hospitalisation Rejected As “Not Medically Necessary”

Another social media complaint reviewed by NewsX points to a similar concern around the basis of claim rejection.

@drprashantmish6 #StarHealthInsurance my father is having fever for last 8 days , fever of more 100°f , needed admission, star health says patient does not need admission, we (star health ) wont pay for same.

For what purpose do we buy medical insurance? pic.twitter.com/RB8PjVA7W4— Naresh Jain (@NareshJ57438) March 22, 2026

In a letter dated March 21, 2026, Star Health informed P.D. Hinduja National Hospital and Medical Research Centre, Mumbai, that it was “unable to admit” the claim request for Laxmilal B. Jain, a 65-year-old insured patient who was hospitalised for fever.

The rejection reason stated that the company was not liable to make payment for “hospitalisation is not medically necessary”.

The issue raised by the case, which another user also shared on X, poses a much broader question. When a patient is admitted into a hospital, such as P.D. Hinduja National Hospital, for fever, and when the doctor treating the patient or the hospital deems admission necessary, on what medical grounds does the insurer subsequently decide the admission wasn’t justified?

This issue is also particularly relevant as claims are often made by policyholders, who state that they are only receiving generic rejection responses, and there is no clear communication of medical reasoning or findings in the assessment.

NewsX Contacted Star Health Customer Care

To better understand Star Health’s claims process, NewsX contacted the company’s customer care team on two separate occasions, posing as a prospective customer.

NewsX based several questions on concerns that existing policyholders had repeatedly raised.

When asked whether a person with a pre-existing disease who is not on medication at the time of policy purchase would be eligible for claims, the representative stated that accident-related injuries are covered from day one and that claims, including those related to pre-existing conditions subject to policy terms, can be made after the activation period.

When asked about claim verification, the representative said a medical expert physically visits hospitals and cross-checks records before processing claims.

The representative also stated that handwritten hospital receipts may be accepted if they are issued on hospital letterheads and carry official stamps.

In another query, NewsX referred to cases where policyholders alleged that claims were denied on the grounds that hospitalisation was “not medically necessary.”

The customer care executive responded that treatment requiring hospitalisation would be considered for claims and that pre- and post-hospitalisation expenses may also be reimbursed following verification.

NewsX also asked whether customers undergo medical screening before policy issuance.

The representative said that no such screening is generally required and that the company relies on medical records and disclosures submitted by customers.

Questions That Remain Unanswered

The conversations raise several questions that extend beyond individual cases.

If Star Health says medical experts physically verify records, what specific discrepancies were discovered in disputed claims, and why were those findings not shared with customers?

If medical history is evaluated when a policy is issued, why do some claim disputes later revolve around information that was allegedly already available to the insurer?

If “misrepresentation of facts” is alleged, should policyholders not be provided with the evidence supporting that conclusion?

Why do some grievance requests seeking clarification reportedly end without detailed written explanations?

If handwritten records from smaller hospitals are acceptable after verification, what standards are applied when determining whether documents are genuine or discrepant?

If a reputed hospital admits a patient for fever, on what documented medical assessment does Star Health conclude that the hospitalisation was “not medically necessary”?

And perhaps most importantly, should an insurer be permitted to cite “multiple discrepancies” without identifying what those discrepancies are when such allegations effectively challenge the authenticity of records issued by doctors and hospitals?

What Do IRDAI Rules Say?

The government’s response in Parliament indicates that insurers are expected to provide detailed reasons for claim rejections.

The measures highlighted by the Finance Ministry include:

- No claim should be repudiated without approval from the Product Management Committee or Claims Review Committee.

- Claims should not be rejected solely because of delayed intimation or lack of documents.

- If a claim is rejected or partially disallowed, insurers must communicate the decision with reference to specific policy terms and conditions

- Timelines for claim settlement have been prescribed.

- Delayed claim settlements can attract penal interest.

The government has also reduced the waiting period for pre-existing diseases from four years to three years under updated regulations.

The Bigger Transparency Question

The issue extends beyond any single policyholder or insurer.

The latest IRDAI data shows that complaints relating to claim handling continue to rise. Nearly half of all insurance complaints now involve claims and related issues. Complaints alleging rejection without reasons are also increasing.

Against that backdrop, the growing number of grievances against Star Health deserves scrutiny.

The fundamental question is not whether insurers should reject claims. Every insurer has a right and obligation to investigate fraud, misrepresentation and policy violations.

The real question is whether policyholders are receiving enough information to understand why a claim was rejected and whether they have been given a fair opportunity to challenge that decision.

When rejection letters cite “multiple discrepancies” or “misrepresentation of facts” but customers say those discrepancies remain unexplained, the claims process undermines trust.

NewsX has reached out to Star Health & Allied Insurance Company seeking its response to the issues raised by policyholders and the questions highlighted in this report. The company will update its response once it receives the information.

Also Read: Exclusive: Delhi Man Alleges Star Health Insurance Rejected Rs 3 Lakh Claim After Years Of Premium Payments

Priyanka Roshan is a business writer and assistant editor at the NewsX website who tracks everything from stock market swings and corporate earnings to personal finance trends and policy shifts. Known for turning fast-moving business developments into sharp, reader-friendly stories, she combines speed, accuracy, and a data-driven approach to break down complex financial news for everyday audiences.

With over 9.5 years of newsroom experience, Priyanka has worked with leading media organisations, including Bussiness, Times Now, and Ping Digital, covering diverse beats such as business, politics, technology, auto, travel, sports, and the world. From live breaking news desks to SEO-led digital storytelling, she specialises in creating engaging content that keeps readers informed without overwhelming them.

The post Star Health Complaints Up 65%: Why Do Claim Rejection Doubts Persist? appeared first on NewsX.

Comments are closed.