Why are thousands of taxpayers revising after filing ITR? Big reason revealed, steps taken to avoid notice

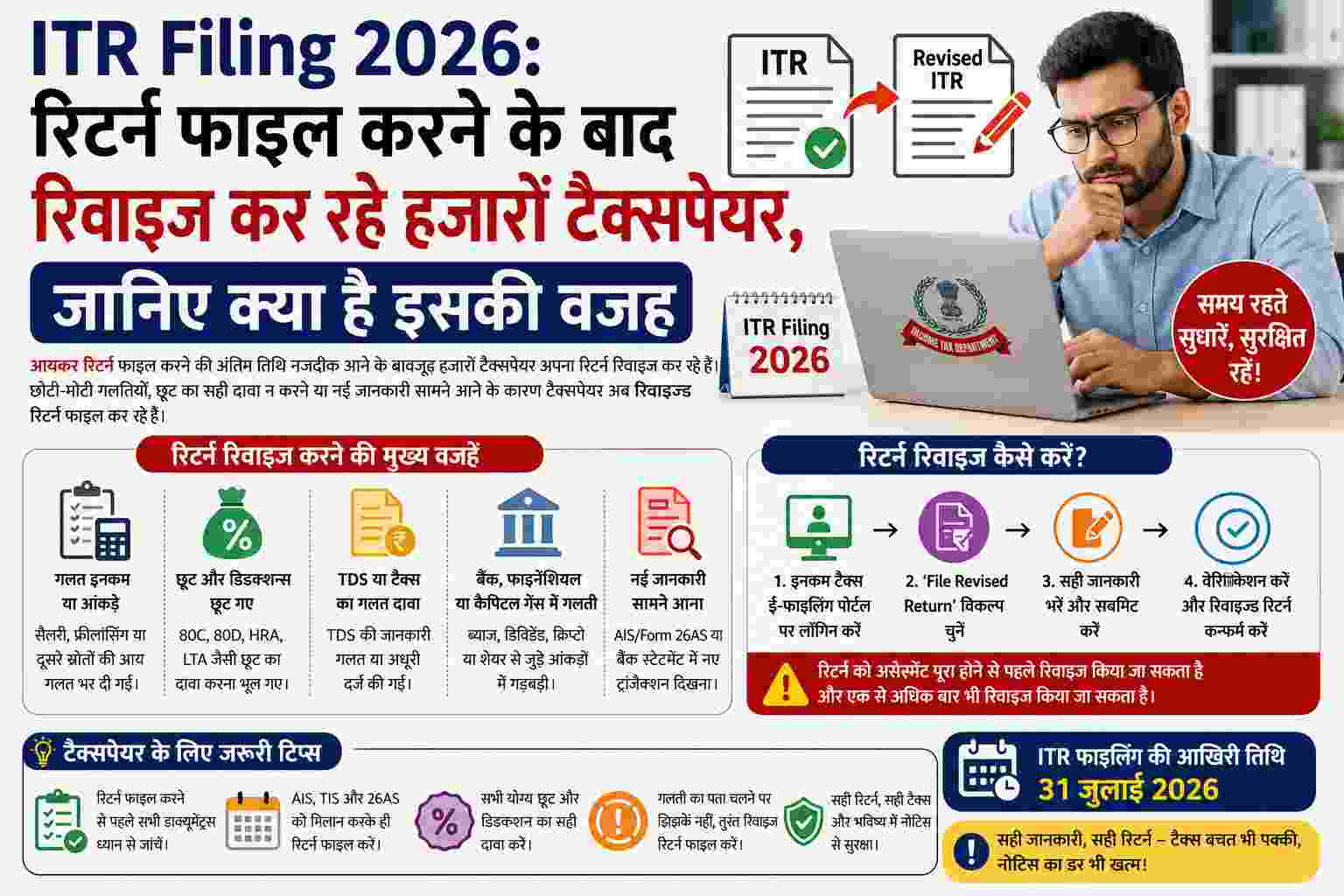

These days a new trend is being seen among the taxpayers filing Income Tax Returns (ITR Filing 2026). There has been an unexpected increase in the number of people ‘revising’ returns after submitting them. The biggest reason for this is the modern technology and data monitoring (Data Analytics) used by the Income Tax Department. The Department now has access to financial information more quickly and comprehensively than ever before. In such a situation, many taxpayers are realizing after filing returns that some of their big transactions have been added to the records later, due to which they have to resort to revised returns to correct their mistakes. The network of data monitoring has increased, new entries are being added to AIS later. The biggest reason behind this entire change is the continuous updating of the Annual Information Statement (AIS). AIS is a digital document that contains a complete log of your entire year’s earnings and major financial transactions. In this, accurate details of your salary, bank interest, purchase and sale of stock market and mutual funds, dividends, foreign currency transactions and any type of capital gain are recorded. The real problem is that AIS is not a static document; It varies with time. Banks, financial companies, and stock brokers update their data with the tax department from time to time. In such a situation, taxpayers who file their ITR in a hurry as soon as the financial year ends, start seeing new entries or new transactions in their AIS after a few weeks. As soon as this difference of data is seen in the system, it becomes very important to file the revised return. AI system is now catching mistakes which were ignored earlier. Today’s Income Tax Department is using state-of-the-art technology, data analytics and faceless scrutiny on a large scale. The department’s automated AI system matches the filed ITR data directly with AIS and Taxpayer Information Summary (TIS). Small discrepancies or financial lapses which could have been ignored in earlier times, are now caught by this system in the blink of an eye. This is the reason why sensible taxpayers are finding it safer to admit their mistake and file the revised return on time, instead of waiting for any strict legal notice or penalty from the department. What are the deadlines for revised returns for assessment year 2026-27? It is important for taxpayers to know that returns for Assessment Year (AY) 2026-27 will still be processed under the old ‘Income Tax Act, 1961’. This rule will remain effective even when the new ‘Income Tax Act, 2025’ has come into force in the country from April 1, 2026. As per the existing rules, the last date for filing revised return without any fee under Section 139(5) of the Income Tax Act is fixed as December 31, 2026. Provided that your assessment has not been completed before this. Big relief proposal: In the Finance Bill 2026, it has been proposed to extend this deadline to 31 March 2027. However, taxpayers may have to pay additional late fees or charges if they file revised returns after the December 2026 deadline. Option to file updated return: If this extended deadline is also missed, then there is a last chance to file ‘Updated Return’ under section 139(8A). This facility is available for 48 months, but you have to pay heavy additional tax and penalty. Why is it wise to file ITR correctly the first time? Adopt this method: The best way to avoid the hassle and mental stress of filing revised returns again and again is to file the correct return with utmost care the first time. For this, before filing ITR, make sure to match all the documents you have with AIS, TIS and Form 26AS. During reconciliation, have your Form 16, bank statement, broker’s P&L statement, interest certificate and capital gain statement in front of you. If you feel that a transaction has been entered incorrectly in your AIS or is not yours, you can immediately raise your objection using the ‘Report Incorrect Information’ facility provided on the portal. Investors in these sectors will have to exercise maximum caution. Taxpayers whose sources of income are limited (such as salary only), do not face much trouble. But people who have multiple sources of income should be especially cautious. Active traders in the stock market, regular investors in mutual funds, those dealing in foreign assets or foreign funds and those earning capital gains from buying and selling of real estate (property) should not lock their returns without cross-verification. A little vigilance on your part can keep you away forever from the hassle of lengthy investigation and notices from the Income Tax Department.

Comments are closed.