EPF vs VPF Calculation: Do this small work as soon as you change jobs, your PF fund will increase 5 times on retirement, know the complete mathematics.

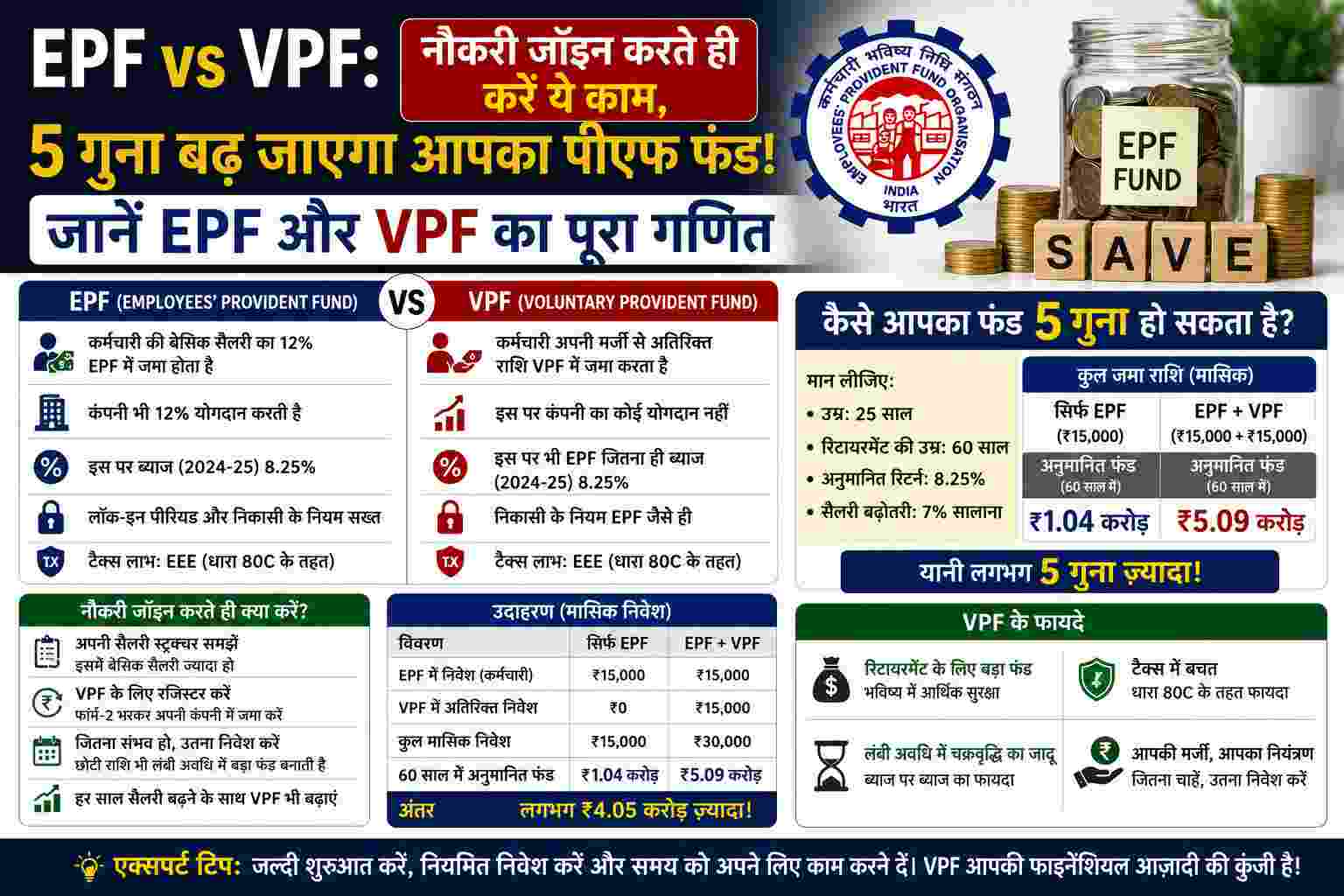

Whenever we get a new job, our entire focus is on the annual CTC and in-hand salary. But do you know that a small portion of your CTC, which goes into the Provident Fund (EPF), can change your entire financial picture after retirement? Often many companies set a minimum government limit of basic salary for calculating EPF contribution, due to which your retirement fund remains very small in the long run. But if you combine Employee Provident Fund (EPF) and Voluntary Provident Fund (VPF) with proper financial planning, then the old age fund can increase up to 5 times and you can easily become the owner of crores of rupees. Let us understand its complete mathematics. How will a fund of ₹ 1.9 crore be created by a small margin? Suppose the annual CTC of an employee is ₹ 12 lakh. Now EPF contribution is decided in two different ways and the difference between the two will surprise you: Case 1: Contribution at minimum limit (monthly saving ₹ 3,600) Most companies deduct 12% EPF only at the government limit of basic salary i.e. ₹ 15,000 per month. In this situation, a total of ₹ 3,600 will be deposited in EPF every month, including your share and the company’s share. If the current interest rate is 8.25% and the investment period is 30 years, then you will get around ₹ 57 lakh on retirement. Case 2: Contribution on actual basic salary (monthly saving ₹12,000) Now suppose your company deducts 12% PF on your actual basic salary, which is 50% of CTC i.e. ₹50,000 per month. In such a situation, the total contribution of you and the company together becomes ₹ 12,000 every month. At this 8.25% interest rate and tenure of 30 years, your total fund will grow to ₹1.9 crore! That is, just by getting PF calculated on basic salary, additional funds of more than ₹ 1.3 crore are added to your pocket without any extra effort. This is the real power of compounding available on PF. VPF will directly take the retirement fund beyond ₹ 3.2 crore. If you want to make your old age more secure and luxurious, then you can opt for VPF (Voluntary Provident Fund). VPF gives you complete freedom to invest in PF as per your wish over and above the mandatory limit of 12%. In the above example, if you invest an additional ₹8,000 through VPF every month along with your EPF contribution of ₹12,000, your total monthly savings will be ₹20,000. After 30 years, at 8.25% interest, your fund will increase to around ₹ 3.2 crore! This is more than 5 times the initial price of ₹57 lakh. While changing or joining a job, pay special attention to these 3 things. The rules for deducting PF and salary structure of every company are different. Therefore, while joining a new job or at the time of salary discussion, definitely check these things: Basis of PF calculation: Clearly ask the HR of the company whether they are contributing PF at the minimum limit of ₹ 15,000 or on your actual basic salary. Share of basic salary: What is the total share of basic salary in your CTC, because your PF fund is decided by this. VPF facility: Does the company allow you to invest extra from your salary through VPF. Important Note: The only direct effect of cutting excess PF and VPF is that it reduces your take-home salary every month. Therefore, before increasing investments for the future, make sure that you have adequate emergency fund ready and that your monthly household expenses are easily met.

Comments are closed.