ITR Filing 2026: Deadline changed after Budget 2026, know which date is the last for you otherwise you will have to pay heavy fine.

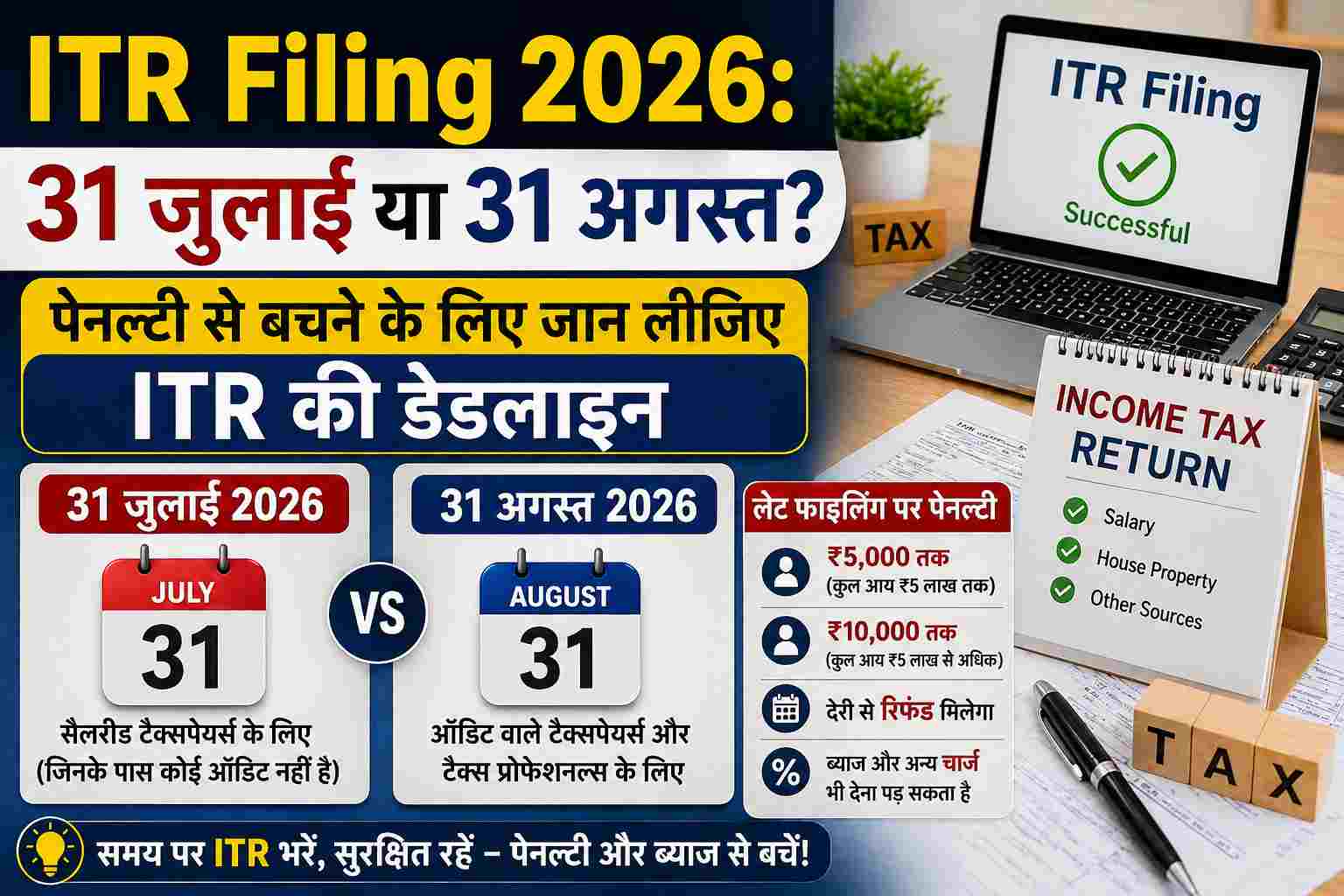

New Delhi: This time major changes have been made in the process of filing Income Tax Return (ITR) for the financial year 2025-26 (assessment year 2026-27). In the budget presented on 1 February 2026, Finance Minister Nirmala Sitharaman has announced new deadlines for different taxpayer categories. If you do not file your return on time, you may not only have to pay a heavy penalty but will also have to pay hefty interest on the outstanding tax. Understand your deadlines as per the category. This time, the government has kept a difference in the dates keeping in mind the convenience of the taxpayers and the complexity of the audit. Note down the last date as per your category: Salaried Class and Pensioners (ITR-1 and ITR-2): If your source of income is only salary, pension, a house or interest, then the last date for you has been fixed as 31st July 2026. Freelancers and Small Businesses (Non-Audit Cases): Professionals or small businessmen whose accounts are not mandated to be audited can file their returns till 31st August 2026. Tax audit matters: For businesses for which audit is required by law, the last date has been kept as 31 October 2026. What are the options if the deadline is missed? If for some reason you are not able to file the return by the stipulated time, then there is no need to panic, but you will have to pay a price for it: Belated Return: You can file your return till 31 December 2026, but in this you will have to pay late fee and interest. Revised Return: If there is any mistake in the filing, then the chance to correct it will be available only till December 31, 2026. Under special circumstances, this time can be extended till March 31, 2027. Updated Return (ITR-U): To show any old income or to correct the mistake, time is available till 4 years after the end of the assessment year i.e. till March 31, 2031. Income Tax Act 2025: Preparation for the future Taxpayers should keep in mind that this year’s filing will be done under the old ‘Income Tax Act 1961’ only. However, the new ‘Income Tax Act 2025’ will become effective from the next financial year (FY 2026-27), for which new forms and rules will be issued before April 1, 2027. Delay can lead to losses. Not filing ITR on time not only attracts penalties, but you are also not able to carry forward your old losses to future years. Also, timely filing eases processes like loan approval and visa application.

Comments are closed.