Stop before taking a personal loan! Are you also making these 4 mistakes? You may have to pay huge damages for years. – ..

In today’s digital era, taking a personal loan has become easier and more convenient than ever. Thanks to the apps of banks and fintech companies, now just one notification comes on your mobile and in a few clicks lakhs of rupees are transferred directly to your bank account. This arrangement seems like a boon when there is a sudden need of money.

But the biggest question that arises here is whether it is right to take the help of personal loan for every small and big need or desire? According to financial experts, the answer is absolutely ‘no’. A personal loan taken at the right time and for the right reason can ease your problems, but a loan taken without thinking or just to fulfill a hobby can completely derail your financial condition for many years.

What is a personal loan and why is it expensive?

Personal loan is called ‘Unsecured Loan’ in financial language. This simply means that to take this loan, you do not have to pledge your house, gold, car or any other asset with the bank. The bank hands over this money to you mainly after looking at your salary, credit score and repayment history.

Since it involves more risk for the bank, its interest rates are much higher than home loan or gold loan. Interest rates on personal loans in the market are generally 10% to 24% or more Can happen. This is why you need to think very deeply before applying for this loan.

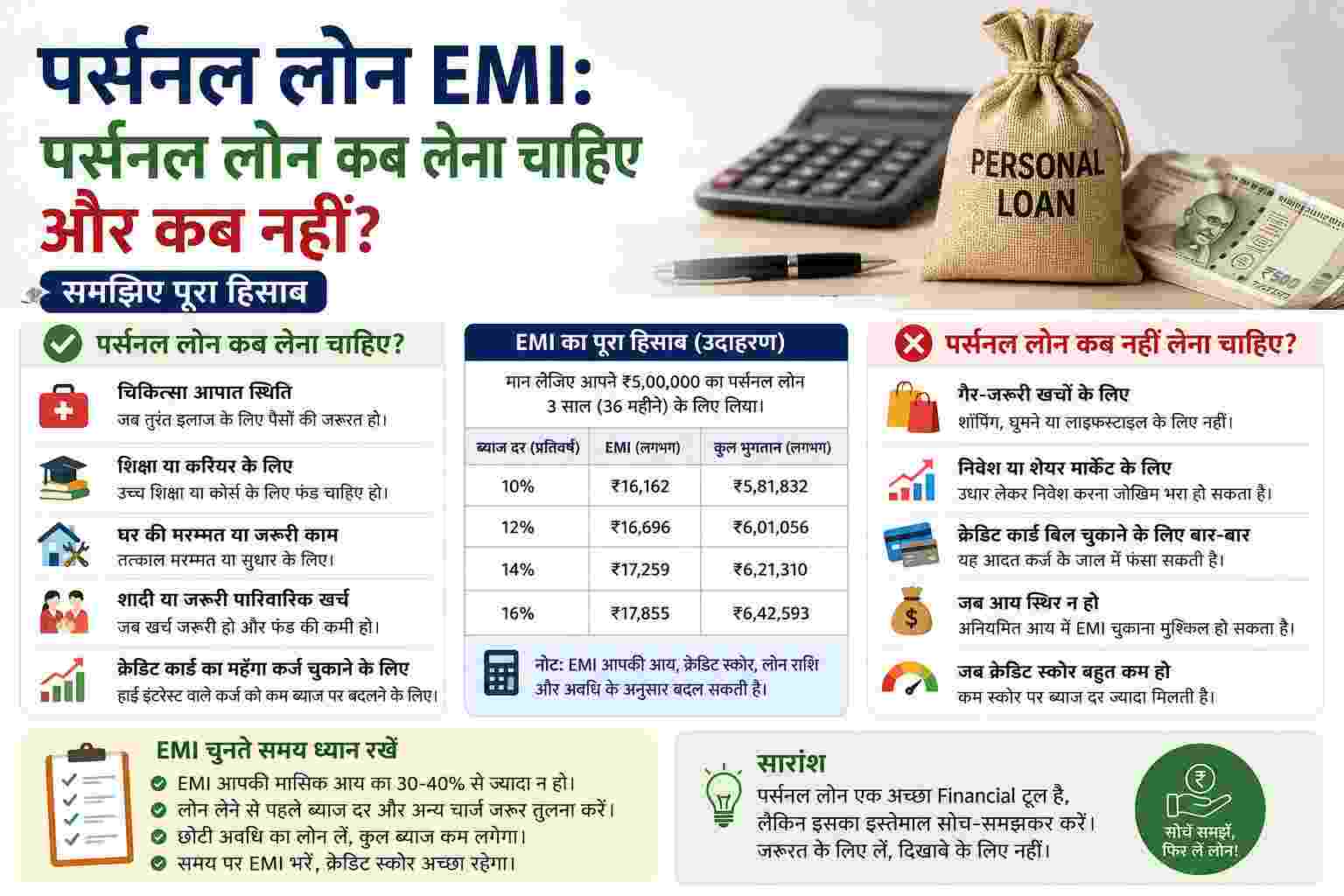

When is it considered wise to take a personal loan?

There are some situations in life where taking a personal loan can prove to be a practical and right step:

-

Medical emergency (sudden illness): If the health of someone in the family suddenly deteriorates and you need money immediately for hospital expenses, then instead of postponing the treatment, taking a personal loan is the best option.

-

Freedom from Expensive Debt (Credit Card Bills): If you have old credit card dues on which the bank is charging 30% to 40% annual interest, then taking a personal loan at a lower interest rate (say 12-14%) is a smart decision to repay that debt.

-

Career and Skill Upgrade: If a particular course, certification or training can take your career to new heights and increase your future income, then a loan can be taken to spend on it. However, if education loan is available, then it should be the first option.

-

Very important home repairs: If your home has a leaking roof, faulty electrical wiring or completely blocked plumbing – something that cannot be avoided, a personal loan can be used to repair it.

Mathematics of personal loan: Understand how much it costs

The real value of a personal loan cannot be understood just by looking at its monthly EMI, but for this you have to look at the total amount to be repaid. Let us understand this with an easy example:

Note: This total expense does not include the processing fee of 1 to 2 percent and hidden charges charged by banks. That is, on a loan of Rs 5 lakh, you pay approximately Rs 2 lakh extra only in the form of interest.

Do not take personal loan for these 4 things even by mistake

avoid these mistakes

-

For travel or vacation: Many people take expensive personal loans to spend holidays abroad. Remember, your trip will end in a few days, but the burden of its EMI will remain on your shoulders for the next 3 to 5 years. One should always save for such things in advance.

-

Extravagance and ostentation in marriage: Getting married by taking a big loan just to get applause from the society or to show off is a very bad financial habit. It is not at all wise to start a new life with a heavy burden of debt.

-

Luxury Gadgets or Lifestyle Products: Taking a personal loan to buy a new iPhone, a big screen TV, or an expensive bike is a loss-making deal, as all these things lose their value over time (Depreciating Assets).

-

Investing in Stock Market or Crypto: Trading in stock market or cryptocurrency with loan money is the most risky. If the market falls, your investment will also sink and you will have to pay the loan EMI from your pocket.

Ask yourself these 3 questions before applying for a loan

If you have decided to take a personal loan, then before making the final signature, ask yourself these three questions with complete honesty:

-

Is this really a need or just a wish?

Often what seems important to us after seeing advertisements is actually just a temporary desire of ours. Learn to understand the difference between the two.

-

Will I be able to pay its EMI without any mental stress?

A basic rule of financial advisors is that the total EMI of all your home loans should be less than your total monthly in-hand salary. Not more than 30% to 40% There should be. If this figure is being exceeded, immediately step back.

-

Is there any cheaper option available in the market?

Before taking a loan, check whether you have an old emergency fund, whether you can get interest-free help from family or a close friend, or whether you can take a low-interest loan against your PF amount or FD. Always choose the option of personal loan only after exploring all avenues.

Comments are closed.